Five reasons for strategic allocation to China A-shares

Five reasons for strategic allocation to China A-shares

As the A-share market opens up to investors and MSCI has taken an additional step to include A-shares, substantial capital flows are again expected to flow into China’s onshore market. Besides this tactical reason to invest in Chinese A-shares, we argue that the market merits longer-term, strategic allocation as well.

Speed read:

- The A-share market is the world’s second largest equity market

- Some of China’s best opportunities are only available in A-shares

- A-shares offer significant diversification benefits and alpha potential

Simply put, the A-share market is too big to ignore. It offers unique investment opportunities that cannot be found in other markets and provides diversification benefits because of its low correlation with the major equity markets, including China’s offshore market. We list five reasons why we believe Chinese A-shares should be part of a portfolio’s strategic allocation.

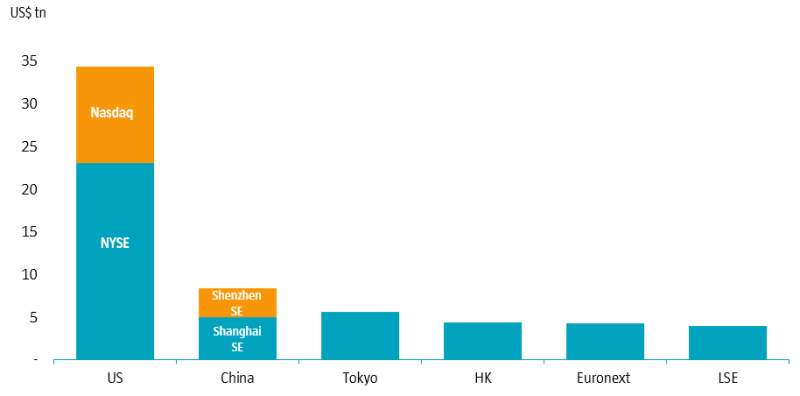

1. The A-share market is the world’s second largest equity market

As Figure 1 shows, the Chinese A-share market – the Shanghai Stock Exchange and the Shenzhen Stock Exchange combined – constitutes the world’s second largest equity market after the US. Its current market capitalization is USD 8.4 trillion.

Figure 1 | Equity markets by market capitalization as at May 2019

Source: Bloomberg, Citi Research

To foreign investors, the A-share market has effectively been a sleeping giant which has largely been ignored. Up until now, this has made sense, given the market’s closed nature; but now that it is opening up, investors can no longer put off deciding whether to invest in this market.

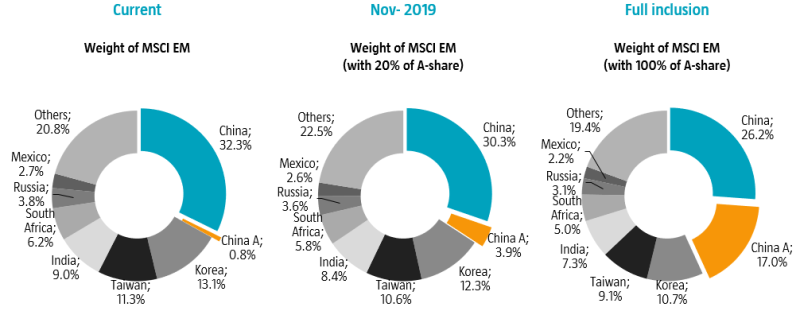

2. MSCI is increasing the A-share weight in its indices this year

This year, MSCI is increasing the weight of Chinese A-shares in the MSCI Emerging Markets Index to 20% inclusion (up from 5% in 2018). This is an important step as we expect it to lead to continuous foreign inflows. Apart from providing evidence of China’s capital market liberalization intentions and of the progress, this will also support the renminbi.

The increasing participation of foreign capital will also create a more balanced investor structure in the market, moving it from retail-dominated to a mix of institutional and retail investors. A higher institutional presence will help to improve corporate governance at A-share listed companies, which we expect will benefit shareholders. Furthermore, the inclusion of A-shares in the relevant indices has made not investing in them an active decision, which for index-aware investors implies taking an active underweight position.

MSCI’s inclusion of A-shares is on the rise

Figure 2 | MSCI China A-share inclusion based on current proposal (as at May 2019)

Source: MSCI, Morgan Stanley Research, Robeco

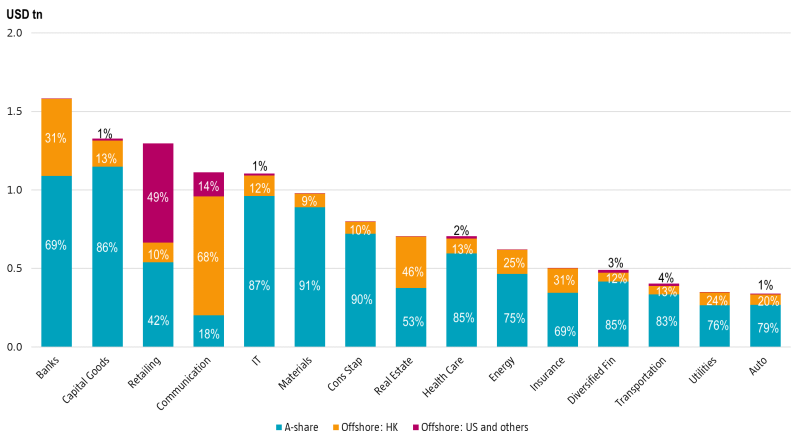

3. Some of China’s biggest opportunities are only available in local markets

The Chinese A-share market accounts for 70% of the market capitalization of all Chinese listed stocks. It offers investors even more diversification potential than offshore H-shares: 10 of the 15 key sectors have over 70% of their market capitalization listed exclusively in China A-shares.

Figure 3 | A-share vs offshore Chinese equities: market cap by sector

Source: wind, Bloomberg, Citi Research, Robeco. Per end of May 2019.

The A-share market offers exposure to state-owned enterprises (SOEs) which we expect to make significant progress in terms of mixed-ownership reforms and improved corporate governance, making them increasingly interesting investment opportunities. The majority of SOEs are part of ‘old economy’ sectors such as materials and energy. Sectors that make up the ‘new economy’ – like healthcare, consumer products, services and technology – have recorded better growth than the market as a whole. These new economy sectors account for around 40% of total A-share market capitalization and represent a large pool of very interesting investment opportunities.

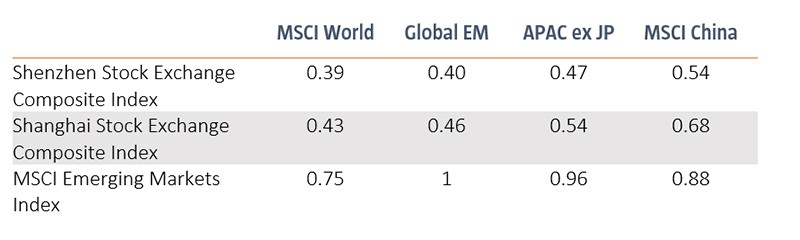

4. Low correlation provides diversification

The Chinese A-share market has a low correlation with global equity markets. One important reason is that it is still largely driven by local retail investors, who hold close to 50% of the market’s total free float market capitalization and account for 80% of total trading volume. Retail investors tend to have a shorter-term investment horizon and behave differently from institutional investors.

A second reason is that the market has long been closed to foreign investors and, therefore, has not moved in step with global sentiment. And while the opening up to foreign investors will eventually increase the market’s correlation with other equity markets, this will take time. Currently, only 3% of market capitalization is foreign-owned, against 30% for Japan and 15% for the US.

Table 1 | Five-year correlation of Chinese A-shares with four major indices

Source: Bloomberg, Morgan Stanley Research. Period: Apr 2014-Mar 2019.

The table shows the five-year correlation between the Shenzhen and Shanghai Stock Exchange Composite Indices and global developed equities, global emerging markets indices, Asia-Pacific ex Japan stocks and the MSCI China Index, which includes only offshore-listed Chinese stocks. For comparison purposes, the table includes the MSCI Emerging Markets Index, which is significantly more correlated to major global markets.

5. Early stage of development offers significant alpha opportunities

The Chinese onshore stock market did not open until 1990 and has only gradually been admitting foreign institutional investors since 2002. This market is set to grow further as corporate earnings improve, more companies are listed, and A-shares become more broadly available to global investors.

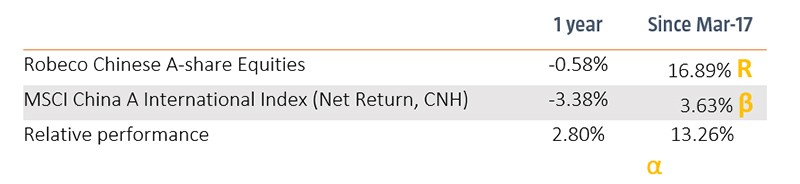

Table 2 shows the return of the Robeco Chinese A-share Equities fund since inception in March 2017 against that of the MSCI China A International Index in the same period. As the track record shows, the A-share market’s structure and predominantly retail ownership offer substantial alpha opportunities. As this will only change gradually, these opportunities will be around for quite some time.

Table 2 | Annualized performance of Robeco Chinese A-share Equities 30/04/2019

Source: Robeco. Figures for Robeco Chinese A-share Equities, gross of fees, based on net asset value, in USD. In reality costs such as management fees and other costs are charged. These have a negative effect on the returns shown. The value of your investment may fluctuate. Results obtained in the past are no guarantee of future performance.

Conclusion

Chinese A-shares are becoming increasingly important for global investors. There are five good reasons why they should be part of a portfolio’s strategic core allocation. Yet, like any other market, the space is not a bed of roses either. It is important to monitor the market closely, and changes in factors such as valuations and earnings will require tactical portfolio adjustments. This, however, does not detract from the strong case for a long-term, strategic position in Chinese A-shares.

- Last:Chinese regulator suspends rating agency over Yongcheng defa 2021/1/2

- Next:THE REAL VALUE OF CHINA'S STOCK MARKET 2020/12/31